Medicare Eligibility in Ohio – Everything You Need to Know

Are you curious about how to qualify for Medicare in Ohio? At RetireMed, we have a dedicated team of knowledgeable advisors in Medicare who have outlined what you need to know about Ohio Medicare eligibility.

Who is eligible for Medicare in Ohio?

Eligibility requirements for Medicare are consistent across the U.S. To qualify for Medicare in Ohio or anywhere in the U.S., you must be a U.S. citizen or permanent legal resident for at least five consecutive years, and you reach Medicare eligibility when at least one of the following applies:

• You are age 65 or older

• You are permanently disabled and have received disability benefits for at least two years

• You have been diagnosed with End-Stage Renal Disease (ESRD) or Amyotrophic Lateral Sclerosis (ALS or Lou Gehrig’s disease)

It’s important to know that there are no income limitations for Ohio Medicare eligibility or Medicare eligibility anywhere else in the U.S.

Medicare in Ohio Explained

Medicare consists of four basic parts: Part A, Part B, Part C, and Part D, which are consistent across the U.S. Depending on your health insurance needs, you can get Medicare coverage through a combination of these parts.

Most individuals qualify for Medicare Part A and Part B when they turn 65, so long as they or their spouse worked at least 10 years (40 quarters) and paid into Social Security taxes. Together, Part A and Part B are considered “Original Medicare.”

Medicare Part C (also called Medicare Advantage) combines Medicare Part A, Part B, and often Part D into one plan. Medicare Part D covers prescription drugs. Part C and Part D offer additional coverage that you can purchase to enhance Original Medicare. While Medicare Part A and Part B are operated by federal and state governments, private insurance companies offer Part C and Part D plans, which are regulated by the federal government.

Medicare Part A in Ohio

Medicare Part A covers inpatient care: hospitalizations, skilled nursing care, hospice, and home health care. Medicare Part A is premium-free for most people. If you or your spouse have worked at least 10 years by the time you turn 65, you receive Medicare Part A at no monthly cost. While you may not owe a monthly Part A premium, you will still pay out-of-pocket costs for medical services.

Medicare Part A costs for 2025

Below are Medicare Part A costs for 2025:

• $1,676 deductible for each benefit period

• Day(s) 1-60: $0 coinsurance for each benefit period

• Days 61-90: $419 coinsurance per day of each benefit period

• Days 91 and beyond: $838 coinsurance per each "lifetime reserve day" after day 90 for each benefit period (up to 60 days over lifetime)

• $0 copay for skilled nursing care days 1-20

• $209.50 coinsurance per day for skilled nursing care days 21-100

• Beyond lifetime reserve days: all costs

Medicare Part B in Ohio

Medicare Part B generally covers two types of medical services: medically necessary services or supplies and preventive services. Some examples include:

• Medically necessary doctors’ services

• Outpatient care

• Preventive services

• Durable medical equipment

• Part-time or intermittent home health and rehabilitative services

A comprehensive list of Medicare Part B coverage can be accessed here.

Medicare Part B costs for 2025

Medicare Part B costs include an annual deductible, a monthly premium, and coinsurance for covered medical services.

• Annual deductible: $257

• Monthly premium: $185 (for most Medicare enrollees)

• Coinsurance: 20 percent of the total cost of covered services

After the annual deductible is met, you typically pay 20% of the cost of services and Medicare covers the rest. When budgeting for your health care expenses, it’s important to note that there is no cap on the 20% that you are responsible for paying.

The Part B costs above apply if your only coverage is Original Medicare (Part A and Part B). One way to lower your out-of-pocket costs is by exploring Medicare Advantage or Medicare Supplement plan options.

Medicare Part C in Ohio

Medicare Part C, also known as Medicare Advantage (MA), offers an alternative to Original Medicare for medical and drug coverage. MA plans are all-inclusive plans offered by private insurance companies that are contracted and approved by Medicare. They roll Part A (hospital-related insurance), Part B (medical insurance), and often Part D (prescription drug coverage) coverage into one plan.

To be eligible for Medicare Part C, you must be enrolled in Medicare Part A and Part B, and be a resident of the Medicare Advantage plan’s service area.

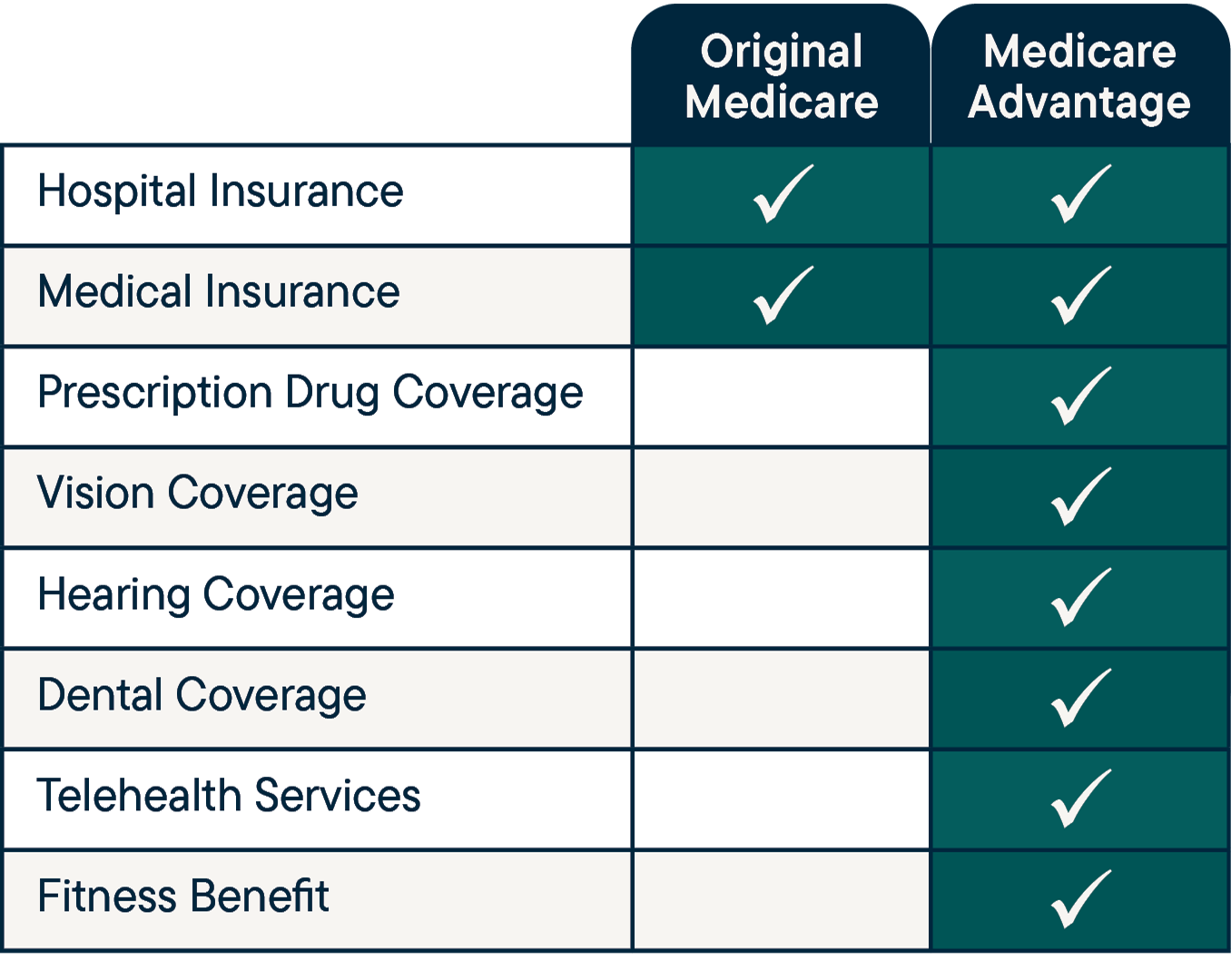

Although MA plans are required to provide the same basic coverage as Medicare Part A and Part B (Original Medicare), these plans also feature extra benefits, such as dental, vision, hearing, fitness memberships, and more. Plans that include prescription drug coverage are referred to as Medicare Advantage Prescription Drug (MAPD) plans. Medicare Advantage plans also cap your out-of-pocket costs for covered services during the plan year.

Below are the standard benefits available on all Medicare Advantage plans compared to Original Medicare.

The amount you pay for a Medicare Advantage plan varies based on the specific plan you select and the benefits it includes. Many plans are available with a low or $0 premium. Regardless of the MA plan you choose, you must continue to pay your Part B premium. When you use MA services, you pay copays, co-insurance, and possibly deductibles.

The amount you pay for a Medicare Advantage plan varies based on the specific plan you select and the benefits it includes. Many plans are available with a low or $0 premium. Regardless of the MA plan you choose, you must continue to pay your Part B premium. When you use MA services, you pay copays, co-insurance, and possibly deductibles.

Medicare Part D in Ohio

You are eligible for Medicare Part D (drug coverage) if you’re eligible for Medicare. You must have Medicare Part A and/or Part B to enroll in Part D.

You can purchase prescription drug coverage in addition to Original Medicare. Standalone Part D plans have a monthly premium. You can save on this monthly premium, however, when you purchase a Medicare Part C (Medicare Advantage) plan, which includes Part D coverage (MAPD).

Medicare Supplement Plans in Ohio

Medicare Supplement plans, also known as Medigap, are health insurance policies sold by private insurance companies. Medicare Supplement insurance is designed to be paired with Medicare Part A and Part B to “fill in the gaps” that Medicare does not cover (such as copays, coinsurance, and deductibles). Many individuals choose Medigap plans because they have very few out-of-pocket costs. However, you will likely pay a much higher monthly premium for a Medicare Supplement compared to a Medicare Advantage plan.

Supplement plans are secondary to Medicare. This means that Medicare pays its share of approved health care costs and then sends the remaining balance to your Supplement insurance company. So long as the services or procedures are qualified, your Supplement will pay most or all of the remaining costs, based on the plan chosen.

It’s important to know that you must be enrolled in Part A and Part B to obtain a Supplement plan. Medicare Supplements do not offer Part D benefits. In order to get prescription drug coverage, enrollment in a standalone Medicare Part D plan or another form of creditable drug coverage (coverage equal to or greater than Medicare’s minimum standards of coverage) is necessary.

How to Apply for Medicare in Ohio

If you qualify for Medicare and are not automatically enrolled, you can sign up for Part A and/or Part B via the online Medicare application, by calling Social Security at 800.772.1213, or by visiting your local Social Security office. If you are coming off group coverage, it’s important to ensure that your Medicare effective date lines up with the end date of your existing insurance coverage.

Most people can apply for Medicare starting three months before their 65th birthday month. Signing up is different if someone has a disability or receives Social Security.

Read more about applying for Medicare in Ohio here.

Questions about Ohio Medicare eligibility? Your local partner in Medicare has answers.

If you have questions about Medicare eligibility or Ohio Medicare plan options, contact our local advisors in Medicare.

Email us at advice@retiremed.com, call us at 866.939.8436, or schedule an appointment to speak with an advisor.

Share This Article